Credit leverage is one of the most powerful — and misunderstood — concepts in finance. At its core, it’s the idea of using borrowed money to amplify returns on investments. For centuries, large corporations, banks, and real estate moguls have used leverage to build wealth at scale. Today, with the right knowledge and access to business credit, entrepreneurs can apply the same principles to grow their businesses and investments faster.

But how exactly do you calculate leverage? What ratios or formulas are used to measure financial leverage? And how do these calculations apply in real-world scenarios like eCommerce, real estate, and investing?

In this article, we’ll break down:

What credit leverage means in finance

The different formulas used to calculate leverage

Examples of leverage calculations in practice

The risks of misusing leverage

How Credit Leverage X helps entrepreneurs apply leverage responsibly

What Is Credit Leverage in Finance?

Credit leverage (also called financial leverage) is the use of borrowed funds — through loans, credit cards, or business credit — to increase the potential return on investment.

The principle is simple:

If the return on investment (ROI) is greater than the cost of borrowing (interest), you profit.

If ROI is less than borrowing costs, you lose.

👉 This is why leverage is often described as a double-edged sword: it multiplies outcomes in both directions.

Why Calculating Leverage Matters

Calculating leverage isn’t just an accounting exercise. It helps answer key financial questions:

Am I borrowing too much?

Ratios reveal whether your debt load is sustainable or risky.

Am I using debt effectively?

Healthy leverage means debt is producing income or appreciating assets.

How will lenders view me?

Banks, investors, and credit issuers rely on leverage ratios to assess risk.

Can I access more funding?

Strong leverage metrics improve your chances of securing higher limits and better rates.

In short: knowing how to calculate credit leverage gives you control over your financial story.

Key Formulas for Calculating Credit Leverage

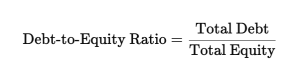

This ratio measures how much debt a company uses compared to its own equity.

Example: If a company has $500,000 in total debt and $250,000 in equity:

This means the company has $2 of debt for every $1 of equity.

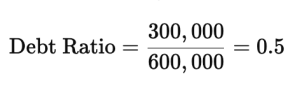

This formula shows how much of a company’s assets are financed through debt.

Example: If a business has $300,000 in debt and $600,000 in assets:

This means 50% of the assets are financed with debt.

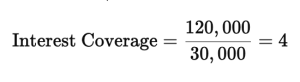

This ratio measures how easily a company can cover its interest expenses with its operating income.

Where EBIT = Earnings Before Interest and Taxes.

Example: If EBIT = $120,000 and interest = $30,000:

This means the company earns 4x its interest obligations — a healthy ratio.

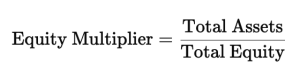

This measures how much a company’s assets are financed by shareholders vs debt.

A higher number signals more leverage.

For individuals, leverage is often measured using debt-to-income:

Lenders prefer DTI below 36%.

Real-World Examples of Credit Leverage Calculations

Example 1: Real Estate Investor

An investor buys a $500,000 property with $100,000 cash and $400,000 borrowed.

Debt-to-Equity = 400,000 ÷ 100,000 = 4.0

Debt Ratio = 400,000 ÷ 500,000 = 0.8 (80%)

👉 High leverage, but common in real estate.

Example 2: eCommerce Entrepreneur

An entrepreneur uses $50,000 in business credit to fund inventory. The business earns $150,000 in sales, with EBIT of $45,000 and $5,000 in interest.

D/E depends on equity (say $25,000): 50,000 ÷ 25,000 = 2.0

Interest Coverage = 45,000 ÷ 5,000 = 9 (very strong)

👉 This is healthy leverage — borrowed money generates much more than it costs.

Risks of Misusing Leverage

While leverage can multiply wealth, it also carries risks:

Over-Leveraging — Borrowing beyond repayment capacity.

Market Volatility — Assets can lose value while debt remains fixed.

Cash Flow Strain — Even profitable ventures can fail if payments outpace cash inflows.

Credit Score Damage — Poor leverage management hurts personal and business credit.

This is why entrepreneurs must monitor leverage ratios regularly and use debt strategically.

How Credit Leverage X Helps Entrepreneurs

At Credit Leverage X, we help entrepreneurs:

Build fundable profiles to qualify for high-limit business credit.

Secure $50,000–$250,000+ in business funding.

Apply leverage strategically to eCommerce, real estate, and digital investments.

Track leverage ratios to ensure healthy borrowing and avoid over-leverage.

The goal isn’t just to get funding — it’s to use leverage as a safe wealth multiplier.

Key Takeaways

Credit leverage = using borrowed money to amplify returns.

Common leverage ratios include D/E, debt-to-assets, interest coverage, and equity multiplier.

Healthy ratios show balance between borrowing and income.

Real-world examples in real estate and eCommerce show how leverage multiplies ROI.

Credit Leverage X provides the mentorship and funding strategies entrepreneurs need to use leverage wisely.

Ready to Leverage Your Credit?

Book a no-cost strategy call and get expert guidance, personalized solutions, and real opportunities to move your goals forward.

Get Started

Frequently Asked Questions