Disclaimer: This article is for educational purposes only and does not constitute financial, legal, or investment advice. Credit Leverage X (CLX) educates and mentors entrepreneurs to help them responsibly access and manage business funding for sustainable growth.

TL;DR

This isn’t a coincidence. It’s a pattern — and it has nothing to do with how hard you work or how much revenue you generate.

Every week, profitable businesses get denied for funding. Operators with $20K, $50K, even $200K in monthly revenue hit a wall when they try to access capital. They assume the numbers will speak for themselves. They don’t.

Lenders don’t fund businesses. They fund fundable profiles. There’s a difference — and most operators don’t learn it until after the rejection letter.

This is the core misconception. Profitable means your revenue exceeds your expenses. Fundable means your business profile satisfies the risk criteria that lenders, underwriters, and automated scoring systems use to make decisions.

Those two things can — and frequently do — exist independently.

A lender evaluating your application isn’t looking at your hustle or your growth trajectory. They’re running your profile against a checklist. If your entity structure is weak, your business credit file is thin, your time in business is under 24 months, or your D-U-N-S number has no trade lines attached to it — the system scores you as high risk. Full stop.

Revenue doesn’t override that. It doesn’t even compensate for it in most automated underwriting environments.

| What You Think Matters | What Lenders Actually Score |

|---|---|

| Monthly revenue | Business credit profile depth |

| Net profit margin | Paydex / Intelliscore / FICO SBSS |

| Client roster or contracts | Time in business (entity age) |

| Personal work ethic | Banking relationship history |

| Business growth rate | Entity structure and compliance |

The SBA’s lending criteria explicitly includes creditworthiness, business financials, and collateral — not revenue momentum. Understanding what underwriters are actually measuring is step one.

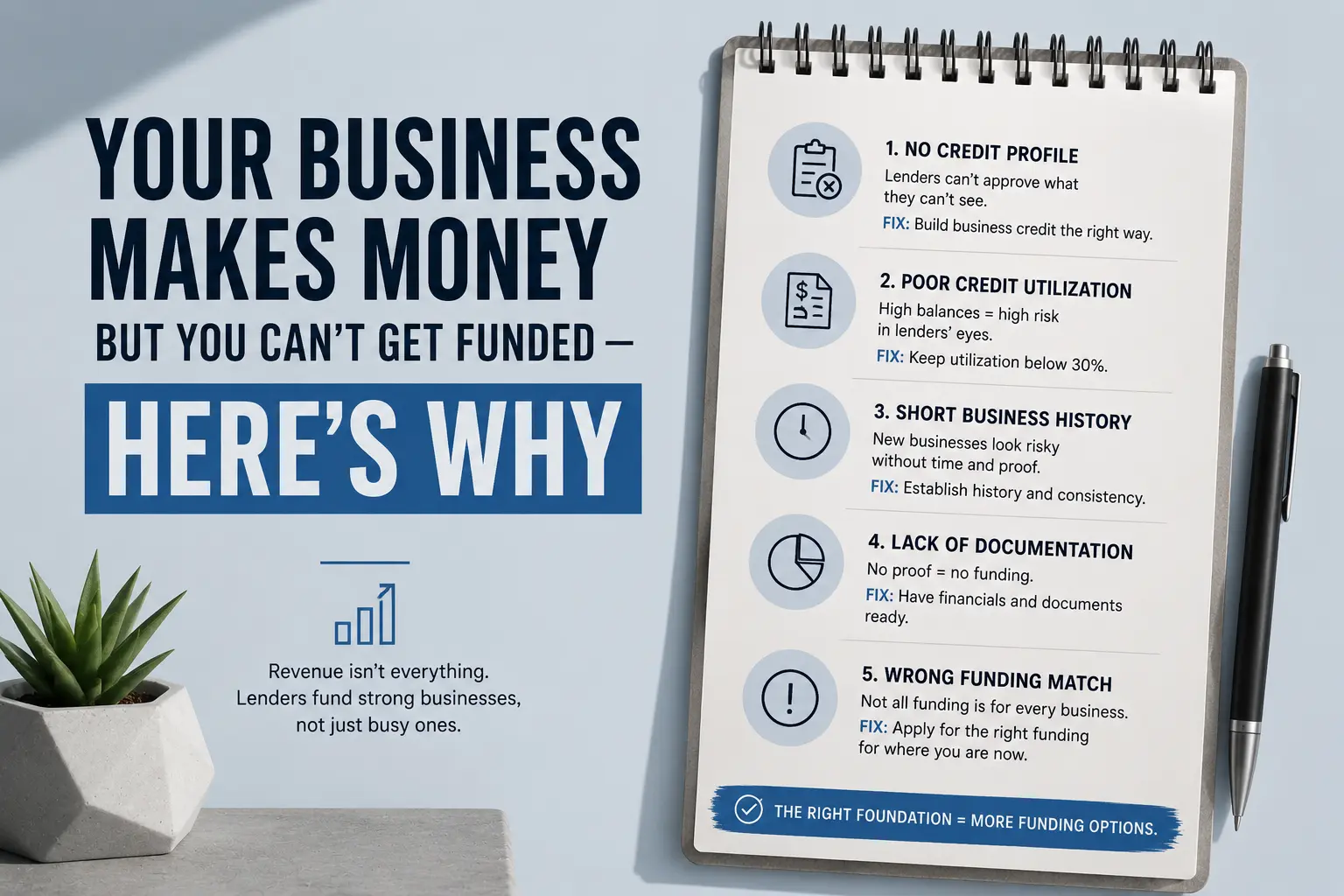

Most denials trace back to one of four structural gaps. Operators rarely see them coming because none of them show up on a profit and loss statement.

1. No Separation Between Personal and Business Credit

If your business doesn’t have its own credit identity — its own profile with Dun & Bradstreet, Experian Business, and Equifax Business — lenders default to your personal credit. That means your personal debt-to-income ratio, personal utilization rate, and personal score are now the underwriting basis for a business funding decision. Even if your personal credit is excellent, this creates a ceiling. Business credit operates on different limits, different scoring logic, and different leverage potential.

2. Thin or Non-Existent Trade Line History

A business credit file with no trade lines is functionally invisible to automated underwriting systems. You need vendor accounts, net-30 accounts, or revolving business credit that reports to the major business bureaus. Without reporting history, there’s no score to evaluate — and no score means no approval at institutional limits.

3. Entity Structure That Signals Risk

Sole proprietorships, recently formed LLCs with no EIN history, or entities that comingle personal and business finances all create red flags at the underwriting stage. Lenders want to see a properly registered entity with a dedicated business bank account, consistent address history, and a matching phone and web presence. These aren’t bureaucratic formalities. They’re trust signals that tell lenders your business exists as a real, standalone operation.

4. Banking History That Doesn’t Support the Ask

If you’re requesting $150K but your business bank account shows irregular deposits, frequent overdrafts, or an average daily balance that doesn’t support the loan amount — the application collapses. Lenders want to see that your banking behavior is consistent with your stated revenue. According to SCORE’s research on small business lending, banking relationship history is a consistent differentiator between approved and denied applicants.

Cash flow-based lenders — merchant cash advance providers, revenue-based financing firms, and some online lenders — have their own denial logic. These lenders are specifically looking at your bank statements, average daily balance, deposit frequency, and net cash flow after obligations.

The operators who get denied here aren’t always unprofitable. They’re often operators whose cash flow pattern looks volatile, even when annual revenue is strong. Seasonal businesses, project-based revenue models, and businesses that run high expenses through the account before showing profit all trigger risk flags in cash flow underwriting.

The fix isn’t cosmetic. It’s behavioral and structural — building a banking profile that matches your actual revenue story.

Operators who access business funding solutions at $50K–$250K levels aren’t necessarily more profitable than the ones who get denied. They’re more prepared.

The distinction comes down to three disciplines:

Business Credit Architecture — They build a business credit profile intentionally, starting with foundation vendors and working toward revolving accounts that report to all three major bureaus. This isn’t passive. It requires sequenced account opening, on-time payment discipline, and monitoring utilization across the business profile.

Entity and Compliance Hygiene — Every detail matches. The business name on the application matches the bank account, the Secretary of State filing, the website, and the Google Business profile. Inconsistencies — even minor ones — create friction in underwriting that kills otherwise strong applications.

Strategic Use of Credit Leverage — Sophisticated operators understand that credit leverage isn’t about borrowing money. It’s about using the structure and positioning of your credit profile to access capital at better terms, higher limits, and lower cost than your competitors. That’s a compounding advantage.

| Factor | Not Ready | Fundable |

|---|---|---|

| Business credit file | No bureaus reporting | 3+ trade lines on all major bureaus |

| Entity structure | Sole prop or new LLC | Established LLC/Corp with EIN history |

| Banking profile | Mixed personal/business | Dedicated account, stable deposits |

| Address/contact info | Inconsistent or personal | Matching across all platforms |

| Business credit score | No score or below 70 Paydex | 80+ Paydex, strong Intelliscore |

You don’t solve a fundability problem by making more money. You solve it by building the profile that matches the capital you want to access.

That means auditing your business credit files across Dun & Bradstreet, Experian Business, and Equifax Business. It means ensuring your entity is compliant and consistent across every public-facing touchpoint. It means understanding how financial leverage works as a tool for scaling — not just a line item on a balance sheet.

The Federal Reserve’s Small Business Credit Survey consistently shows that the businesses with the highest approval rates aren’t the most profitable — they’re the ones with the strongest credit profiles and the most complete applications. Preparation is the differentiator.

Stop applying and getting rejected. Start building the profile that makes approval the expected outcome — not the exception.

Profitability measures income versus expenses. Fundability measures how your business profile scores against lender criteria — including business credit history, entity structure, banking behavior, and time in business. A profitable business with no business credit file or weak entity structure will fail underwriting regardless of revenue.

A business credit profile is your company’s standalone credit identity, separate from your personal credit. It’s tracked by Dun & Bradstreet (Paydex), Experian Business (Intelliscore), and Equifax Business. Lenders use it to assess risk without relying on your personal credit. No profile means no institutional funding at meaningful limits.

Cash flow lenders analyze your bank statement patterns — average daily balance, deposit frequency, overdraft history, and net cash flow. Strong annual revenue with volatile monthly deposits, low average balances, or NSF incidents will trigger denials. The banking profile has to match the revenue story you’re presenting.

With intentional sequencing — starting with foundation vendors that report to business bureaus, then layering revolving accounts — most operators can build a scoreable, fundable profile within 6 to 12 months. Skipping steps or opening accounts that don’t report to bureaus wastes time without building the file.

Yes — if your business credit profile is strong enough to stand on its own. Business credit-based funding evaluates your business file, not your personal score. This is one of the core advantages of building a separate business credit identity. Operators who leverage this correctly access capital at limits that personal credit alone would never support.

A better credit score starts with the right strategy. Let Credit Leverage X help you take control of your finances, improve your credit, and unlock the funding you deserve.

Start Your Credit Strategy

Subscribe now to keep reading and get access to the full archive.