Disclaimer: This article is for educational purposes only and should not be taken as financial or legal advice. Credit Leverage X (CLX) provides business credit mentorship and education to help entrepreneurs build, protect, and leverage credit responsibly. Always consult a financial professional before making credit or funding decisions.

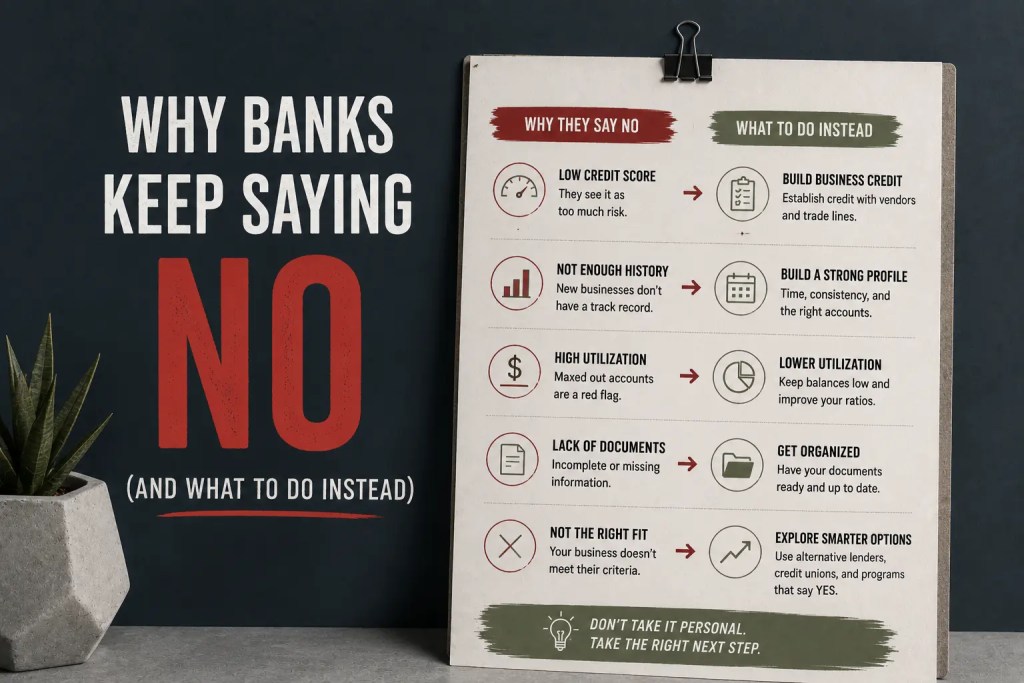

If you want to build strong business credit, you’ll need more than just an EIN or LLC — you need vendor accounts that report to the business credit bureaus, especially Dun & Bradstreet (D&B).

These vendors act as the first stepping stones in your business credit journey. They provide products or services on Net-30 or Net-60 terms (giving you 30–60 days to pay your invoice) — and when you pay on time, they report your positive payment history to credit bureaus.

The result? You begin to build a PAYDEX score, D&B’s equivalent of a business credit score.

At Credit Leverage X (CLX), we teach clients how to strategically use these vendor accounts to build their business credit profile from the ground up — even with zero prior credit history.

This guide covers the best vendor accounts in 2025 that report to D&B, how to get approved, and how to use them effectively for maximum funding potential.

A vendor account (also known as a Net-30 account) allows your business to purchase goods or services now and pay later — typically within 30 days.

These accounts:

Unlike traditional financing, vendor credit is easier to obtain for new businesses — even without revenue or a personal guarantee — as long as your company is structured properly.

Dun & Bradstreet (D&B) is the largest and most influential business credit reporting agency in the U.S. It issues the D-U-N-S Number — your business’s official credit identifier — and compiles your PAYDEX score based on trade line activity.

PAYDEX scores range from 0 to 100, where:

The higher your score, the more likely lenders and suppliers will trust your business with larger credit limits and favorable terms.

CLX Tip: Your goal is to establish at least 3–5 vendor accounts that report to D&B before applying for revolving business credit cards or funding.

Here’s how the vendor reporting process works step-by-step:

This process signals to lenders that your business is trustworthy and capable of managing debt responsibly.

Here’s an updated list of vendor accounts verified to report to D&B (and often other bureaus) — ideal for new businesses building credit in 2025.

Reports To: D&B, Experian Business

Type: Shipping, warehouse, and packaging supplies

Requirements:

Reports To: D&B

Type: Office and cleaning supplies

Requirements:

Reports To: D&B, Equifax Business

Type: Industrial supplies, tools, and safety equipment

Requirements:

Reports To: D&B, Experian Business, Equifax Business

Type: Office and educational supplies

Requirements:

Reports To: Equifax and D&B

Type: Office, tech, and educational materials

Requirements:

Reports To: D&B

Type: Industrial and maintenance supplies

Requirements:

Reports To: D&B, Equifax Business

Type: Tech software, training, and cybersecurity

Requirements:

Reports To: D&B, Experian Business

Type: Business planning and consulting services

Requirements:

Works best for professional service firms or new startups seeking credibility

CLX Tip: Use this vendor to add diversity to your tradeline mix beyond physical supplies.

To generate your first D&B PAYDEX score, you need:

CLX Funding Formula:

✅ 5–7 vendor accounts → ✅ PAYDEX score → ✅ Store cards → ✅ Revolving credit → ✅ $50K–$250K in funding

Consistency is key — it’s not about how much you spend, but how consistently you pay early.

Building business credit isn’t just about opening accounts — it’s about using them the right way.

Graduate to higher tiers. Once your vendors report, apply for revolving store and business cards.

At Credit Leverage X, we teach entrepreneurs how to build business credit systematically and strategically — not through guesswork.

Our mentorship includes:

By following CLX’s proven process, clients can build fundable business credit in 3–6 months and unlock six-figure financing with confidence.

Book a no-cost strategy call and get expert guidance, personalized solutions, and real opportunities to move your goals forward.

Get StartedNo. Many vendors offer Net-30 terms but do not report — always verify reporting policies before opening an account.

Yes. With a properly structured business and EIN, you can build credit solely under your business entity.

Typically 30–90 days after your first on-time payment.

Absolutely. They establish your credit foundation — a prerequisite for business loans, lines of credit, and 0% funding approvals.

A better credit score starts with the right strategy. Let Credit Leverage X help you take control of your finances, improve your credit, and unlock the funding you deserve.

Start Your Credit Strategy

Subscribe now to keep reading and get access to the full archive.